Topic pillar

Reporting and Disclosure

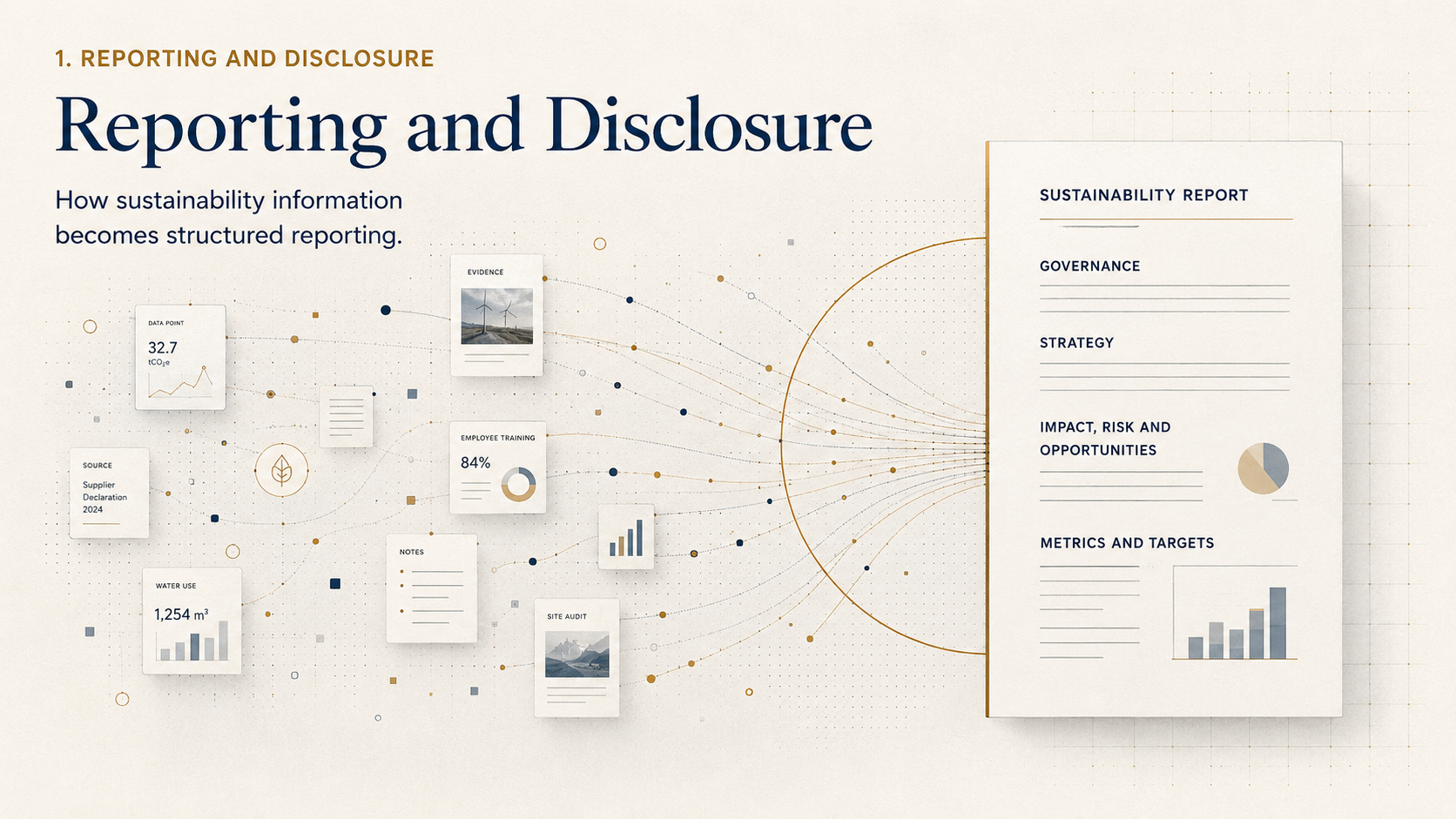

The architecture of what gets said, what gets left out, and why.

A sustainability report is not a summary of good intentions. It is a structured argument with boundaries, and every boundary is a decision. This pillar examines how CSRD, ESRS, and disclosure frameworks turn a year of activity into a document that can be tested — and what gets lost when reporting becomes decoration.

Two lenses, same map. Topics are the disciplines. Pillars (CSRD, EUDR) are the regulations they're tested under.

Why this matters

A sustainability report is a structured argument, not a summary. Every number in it implies a boundary, a method, and an audience that can question both.

When reporting frameworks change, the harder shift is rarely the data — it is the discipline of deciding what to include, what to leave out, and how to defend each choice.

Disclosure earns trust when it is selective for the right reasons: relevance to decisions, traceability of evidence, and honest treatment of what is not yet known.

Common misunderstandings

Where careful readers slow down.

“More data means better disclosure.”

ClarificationOnly if the data supports a bounded claim and can be traced to a credible source. Volume without structure adds noise, not assurance.

“If a metric exists in the standard, we have to report it.”

ClarificationStandards expect a materiality argument first. Reporting a non-material data point as if it were material weakens the rest of the report.

“Digital tagging is a formatting step.”

ClarificationTagging is a disclosure decision. Each tag commits to a definition and a boundary that reviewers and regulators will read literally.

“Our sustainability report and our CSRD statement can be the same document.”

ClarificationThey serve different audiences and different evidentiary thresholds. Conflating them tends to weaken both.

Key subtopics

The lines of inquiry beneath this pillar.

Evidence discipline

What evidence discipline reporting requires

Reporting evidence is documentary first: methodologies, scoping notes, data lineage, and a register of judgements made under uncertainty. Anything that ends up in the published report should be traceable back to a working file a reviewer can read.

The discipline is to write the disclosure and the evidence trail together, not to assemble the trail after the narrative is fixed. When the two diverge, the report becomes a marketing artefact regardless of intent.

Frameworks it touches

This discipline shows up in regulation. Below are the framework pillars where it is operationalised — each one is the same map seen from the rule-maker's side of the table.

Articles in this topic

The pages on this site that sit inside this territory.

Related essays

Read these alongside this pillar.

Continue across pillars