Topic pillar

Materiality and Decision-Making

Deciding what matters enough to be counted — and what doesn't.

Materiality is not a content exercise. It is a discipline of deciding which topics are decision-relevant, on what evidence, and with what reasoning. This pillar covers double materiality, impact and financial lenses, and how a materiality assessment becomes a record that an auditor or regulator can retrace.

Two lenses, same map. Topics are the disciplines. Pillars (CSRD, EUDR) are the regulations they're tested under.

Why this matters

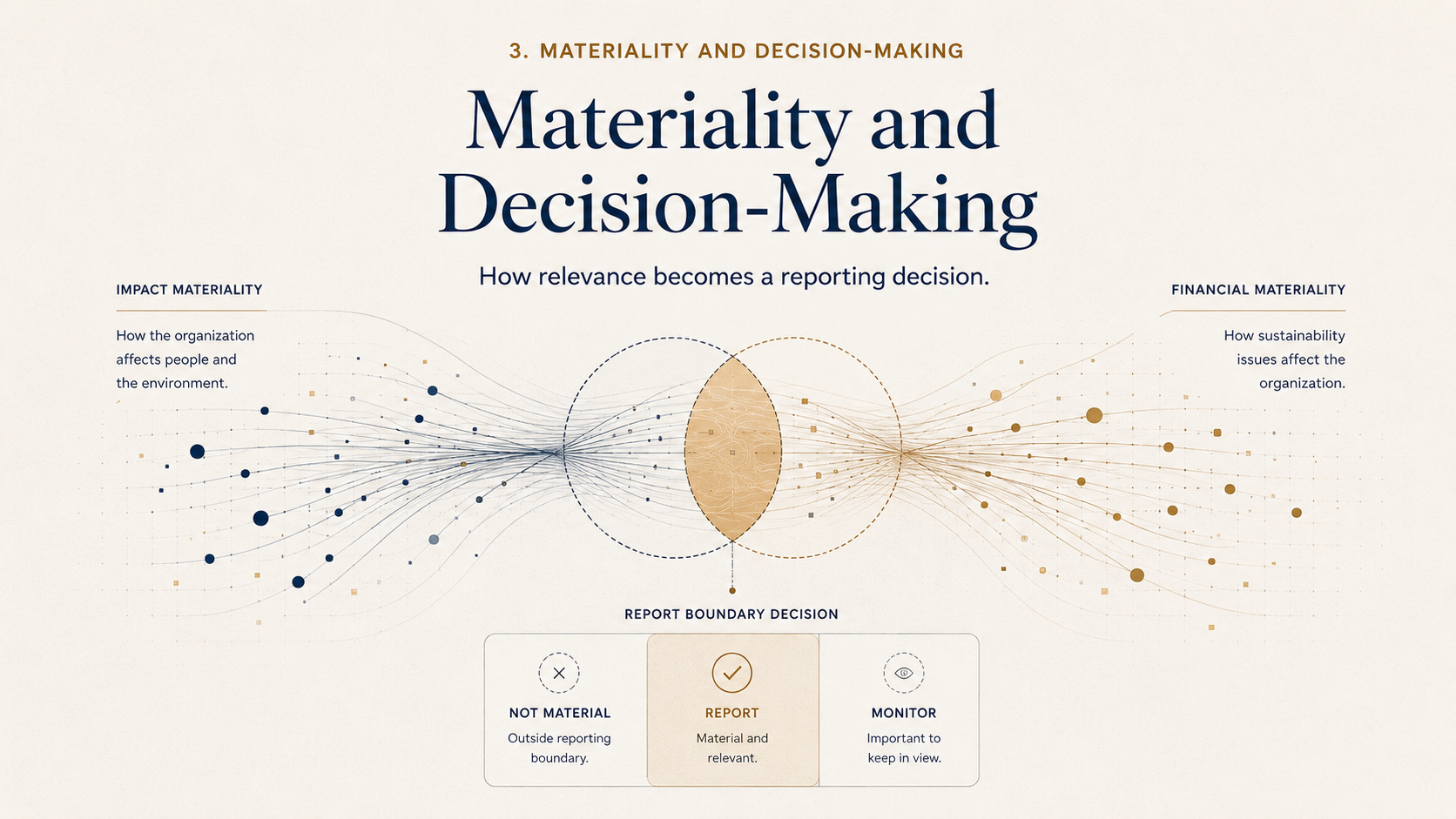

A materiality assessment is a record of choices, not a survey result. Each topic kept or removed is a defensible decision that an auditor or regulator can re-trace.

Double materiality forces two questions in parallel: how the world acts on the company, and how the company acts on the world. The discipline is to answer both with the same rigour.

Decision-useful disclosure begins with naming the decision the reader is being helped to make. Without that, materiality becomes a discussion about topics in the abstract.

Common misunderstandings

Where careful readers slow down.

“We surveyed stakeholders, so our materiality assessment is done.”

ClarificationStakeholder input is one signal. Materiality is the company’s reasoned conclusion about what is decision-relevant, given that input and other evidence.

“Double materiality just means doing materiality twice.”

ClarificationIt is one integrated assessment with two lenses applied together: impact materiality and financial materiality, often on overlapping topics.

“If a topic is material to peers, it is material to us.”

ClarificationPeer benchmarking is a sanity check, not a conclusion. Materiality has to follow your own activities, exposures, and stakeholders.

“Materiality is settled once a year.”

ClarificationIt is revisited whenever the business, the value chain, or the regulatory expectation shifts. The assessment is a living artefact.

Key subtopics

The lines of inquiry beneath this pillar.

Evidence discipline

What evidence discipline materiality requires

Materiality evidence is the record of the decision: which topics were considered, which were retained, what evidence supported each call, and which stakeholders were consulted under what method.

The discipline is to write the conclusion and the working memo together. The published list of material topics should be the executive summary of a file an auditor can actually read.

Frameworks it touches

This discipline shows up in regulation. Below are the framework pillars where it is operationalised — each one is the same map seen from the rule-maker's side of the table.

Articles in this topic

The pages on this site that sit inside this territory.

Related essays

Read these alongside this pillar.

Continue across pillars